Table of Contents

To filter and select the best strategies from your 300+ strategies in Portfolio Master, follow a systematic approach that aligns with your ranking criteria and ensures that only the most robust and stable strategies are included in the final portfolio. Here’s a step-by-step guide to filtering:

1. Apply Your Ranking Criteria

Use the criteria you’ve already set for ranking individual strategies: – CAGR/Max DD% > 1 – Sharpe Ratio > 2 – Profit Factor > 1.5 – Stability > 0.8 – Open DD% < 15%

This initial filter should remove many strategies that don’t meet the baseline performance requirements.

2. Check In-Sample (IS) and Out-of-Sample (OOS) Performance

- IS Testing: Review the performance of each strategy during the in-sample period to ensure that it was optimized correctly.

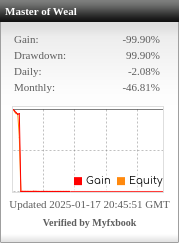

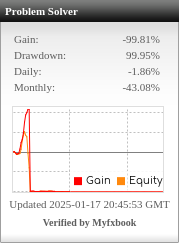

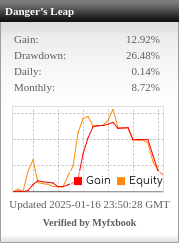

- OOS Testing: More importantly, assess the performance during out-of-sample testing to ensure the strategy is robust in unseen market conditions. Strategies with a high OOS Sharpe ratio and low OOS drawdowns are more likely to perform well in live trading.

3. Evaluate Strategy Correlation

- Use correlation analysis to ensure that strategies in your portfolio are not highly correlated. Highly correlated strategies expose you to similar risks across multiple strategies, increasing the chances of simultaneous drawdowns.

- Keep strategies with low or negative correlation in your portfolio to achieve diversification and reduce risk.

4. Monte Carlo Simulations

- Perform Monte Carlo stress tests on your selected strategies to assess how they handle market noise and randomness. Strategies that consistently perform well under Monte Carlo simulations are more robust.

- Focus on strategies with a low chance of ruin and those that maintain good metrics like Sharpe ratio and Profit Factor in the simulated results.

5. Examine Trade Frequency and Conditions

- Look for strategies that maintain consistent trade frequency and avoid excessive overtrading, which can increase transaction costs and slippage.

- Ensure that strategies follow a balance of trend-following, breakout, and swing trading methodologies (as you’ve chosen) to reduce dependency on a single market condition.

6. Filter for Drawdown Recovery

- Evaluate how fast each strategy recovers from drawdowns. Strategies that recover quickly are generally more reliable for long-term use. Use the drawdown recovery time as an additional filter.

7. Forward Testing

- Take your top strategies and conduct a small-scale forward testing or paper trading to see how they behave in current market conditions. Live market dynamics often differ from historical data, so this step is crucial for final validation.

8. Select a Balanced Portfolio

- After narrowing down the best-performing strategies, use Portfolio Master to combine them into an optimized portfolio with diverse market exposures and timeframes (H1/H4, M15/H4, etc.).

- Make sure the combined strategies adhere to your risk management rules, such as RRR > 1:3, duplicate orders, closing positions on Fridays, and break-even trailing stops.

9. Monitor Ongoing Performance

- Continue to monitor the performance of your portfolio once it’s live, making adjustments only if necessary. Pay attention to how strategies perform during different market phases (trending, ranging, volatile) to ensure long-term stability.

By following this structured filtering process, you’ll be able to select a portfolio of strategies that not only meet your criteria but are also robust, diversified, and ready for live trading.