performance.")

OOS Testing: More importantly, assess the performance during out-of-sample testing to ensure the strategy is robust in unseen market conditions. Strategies with a high OOS Sharpe ratio and low OOS drawdowns are more likely to perform well in live trading.

this OOS should be > ?

When assessing out-of-sample (OOS) performance, the following benchmarks can help determine if a strategy is robust enough for live trading:

1. OOS Sharpe Ratio:

- A Sharpe ratio greater than 1 indicates that the strategy has delivered excess returns relative to its volatility.

- A Sharpe ratio of greater than 2 is considered excellent, suggesting strong performance and favorable risk-adjusted returns.

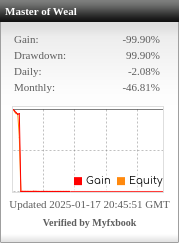

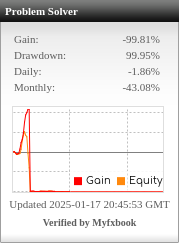

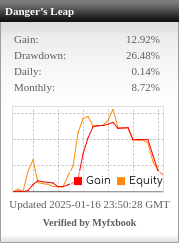

2. OOS Drawdown:

- Aim for a maximum drawdown of less than 15%. This benchmark helps ensure that the strategy does not experience severe losses that could jeopardize the trading account.

- Additionally, the recovery time from drawdown is important; faster recovery is generally preferable.

3. Profit Factor:

- A profit factor greater than 1.5 is generally favorable. This means that the strategy makes 1.5 times more profit than it loses.

4. Consistency:

- Look for consistency in OOS performance metrics, such as stable returns and low volatility, over a sufficient sample size (e.g., at least 6-12 months of trading).

Summary:

- OOS Sharpe Ratio > 1 (ideally > 2)

- Maximum OOS Drawdown < 15%

- Profit Factor > 1.5

Meeting these benchmarks can indicate that the strategy is likely to perform well in live trading.